Oura’s confidential IPO filing and reported $11 billion valuation may look like a wearable hardware milestone.

They are more than that.

They are a live stress test for how technology companies turn commoditized sensors into defensible, recurring value. The smart ring market is not simply an engineering race; it is a textbook case study in the Scenario Maturity Assessment Framework (SMAF).

Hardware captures attention. Scenario captures lifetime value.

This is why smart rings are a powerful case study for the Scenario Maturity Assessment Framework — SMAF Compass™.

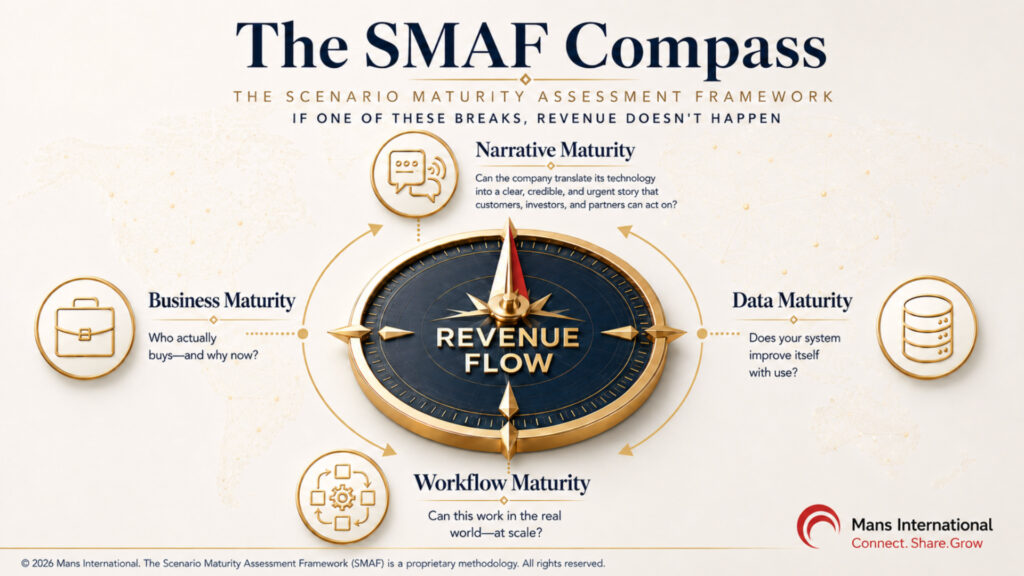

The Four Pillars of the SMAF Compass

Founders do not usually fail because their technology is weak. They fail because they try to execute a strategy that the market scenario is not mature enough to support.

This is the core logic behind the SMAF Compass™, developed by Mans International: a strategic lens for evaluating whether a specific commercial scenario can convert technology into trust, usage, revenue, and defensible value.

At a public level, the framework examines four visible dimensions of scenario maturity:

Narrative Maturity: Can the company translate complex tech into a clear, credible, and urgent story that customers, investors, and partners act on?

Business Maturity: Who actually buys — and why now? Is the pricing model aligned with user tolerance?

Workflow Maturity: Can this work in the real world — at scale — without friction?

Data Maturity: Does the system improve itself with use? Does data create an escalating switching cost?

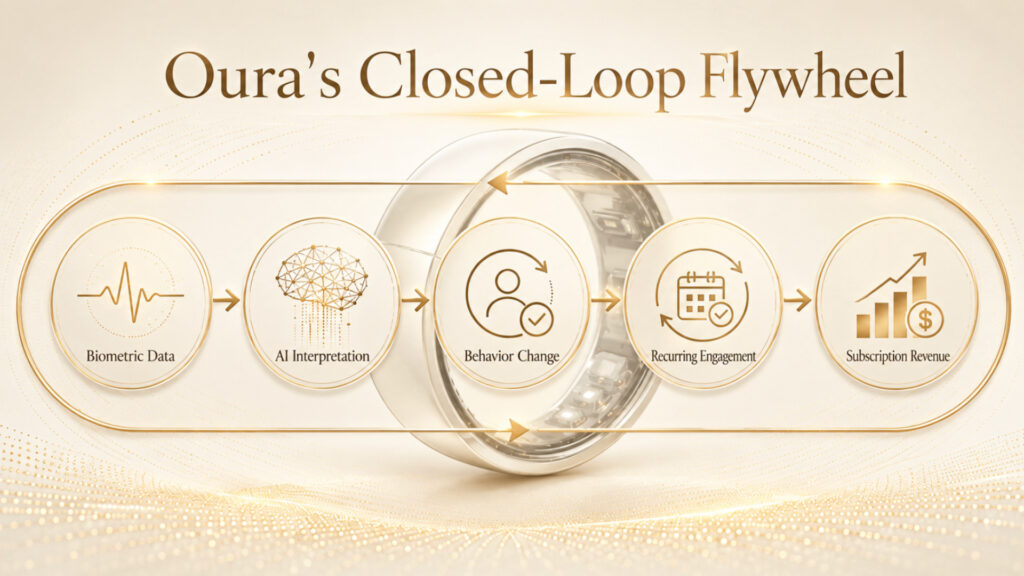

1. Oura’s Real Moat Is Not Titanium. It Is Data & Narrative Maturity.

Oura did not become valuable because it built a beautiful ring. The ring is merely the physical entry point. The intelligence layer is the actual business.

Oura’s projected 2026 revenue of $1.5 billion to $2 billion, with an estimated 80/20 hardware-to-SaaS mix, proves its mastery of the SMAF engine:

- Narrative & Business Maturity: Oura shifted the story from “step counting” to “readiness and recovery.” Its $5.99/month subscription model is a strategic bet that users will pay continuously if the product helps them decode their own bodies.

- Data & Workflow Maturity: This creates a closed-loop flywheel: Biometric Data → AI Interpretation → Behaviour Change → Recurring Engagement → Subscription Revenue

Break any link, and the model collapses. If the insight is generic (Data failure), the habit does not form (Workflow failure), subscription churn rises, and the R&D flywheel slows. Oura’s IPO validates that consumer health hardware can achieve full SMAF alignment.

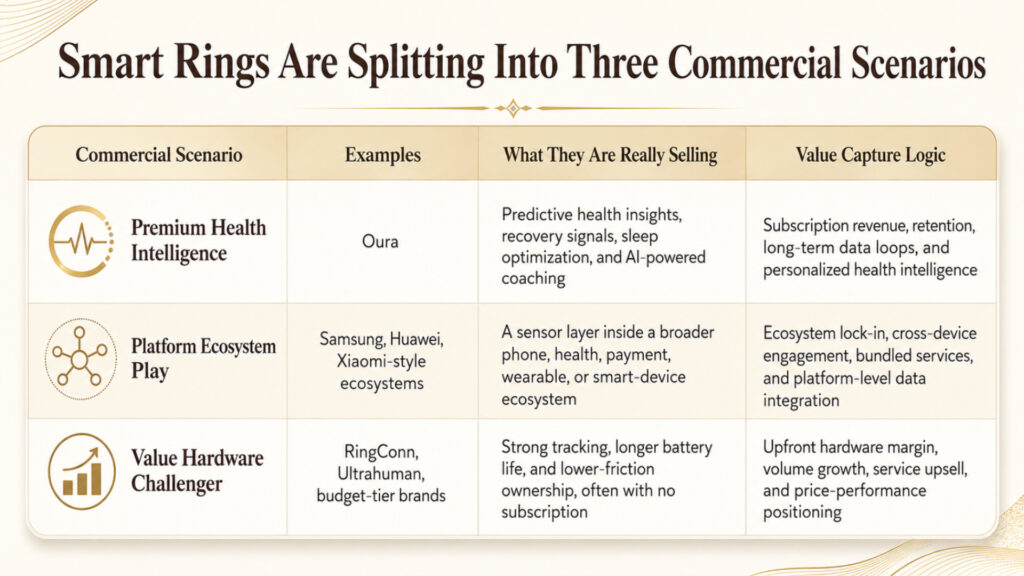

2. Smart Rings Are Splitting Into Three Commercial Scenarios

The mistake many founders make is treating smart rings as a single market. They are not. The same form factor now supports three distinct commercial scenarios, each requiring a different maturity foundation:

The danger for founders isn’t choosing the wrong product; it’s choosing a business model that their specific scenario cannot support.

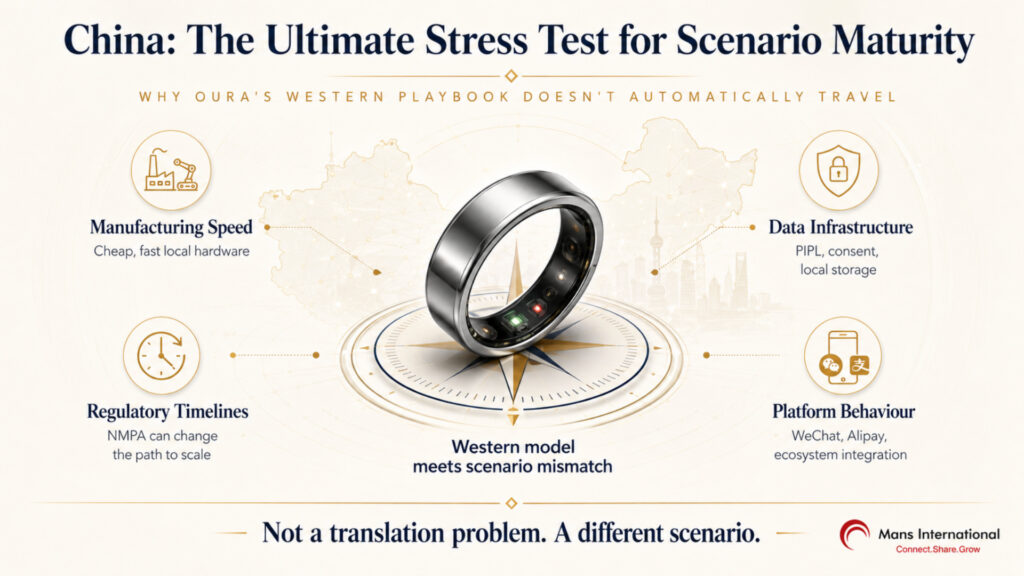

3. China: The Ultimate Stress Test for Scenario Maturity

China makes the necessity of the SMAF visible. Oura’s limited active presence in the region is not a market oversight — it is a profound scenario mismatch.

While Oura’s model thrives in the West’s personal health intelligence scenario, attempting to port it to China causes the SMAF compass to spin wildly. The market sits at the intersection of four unique forces — manufacturing speed, data infrastructure, regulatory complexity, and platform behaviour — each demanding a completely reconfigured playbook:

1. Business Maturity (Manufacturing Speed & Subscription Friction):

Western consumers accept buying a premium device and paying a monthly fee. A Chinese consumer asks: Why pay a subscription after buying the hardware? This resistance is compounded by Shenzhen’s ODM (Original Design Manufacturer) infrastructure, which allows local competitors to move from concept to a functional commercial product with low seed capital. When local hardware is cheap and fast, competing on hardware margins alone collapses into a race to zero.

2. Data Maturity (The PIPL Wall):

Health data is not ordinary data. China’s Personal Information Protection Law (PIPL) and Data Security Law create strict boundaries around biometric information, local storage, consent, and cross-border transfer. A foreign healthtech company cannot simply import its Western cloud architecture and expect its data loop to function legally.

3. Workflow Maturity (Regulatory Timelines):

Regulation dictates scale. If a smart ring’s claims move from wellness tracking into diagnostic utility, the product may trigger China’s NMPA medical device pathway. That abruptly changes the entire commercialization timeline, adding massive friction to real-world workflow and deployment.

4. Narrative Maturity (The Ecosystem Node):

Chinese digital behaviour is deeply ecosystem-driven. Consumers expect seamless, free integration with WeChat, Alipay, domestic smartphone ecosystems, and local fitness communities. To win, a company’s narrative must shift from selling a standalone “individual health tracker” to offering an “ambient digital node.”

This is why Oura’s Western strategy does not automatically travel. Its subscription strategy is powerful in a market where users value individualized health coaching and accept monthly digital services.

But in China, a winning strategy requires a completely redesigned scenario: free core features, localized data infrastructure, native ecosystem integration, regulatory clarity, and tiered monetization.

That is not a translation problem. It is a different scenario.

Closing: The Ring Is Only the Surface

The smart ring market is not rewarding the company with the sleekest hardware alone.

It is rewarding the company that understands how a device becomes a habit, how a habit becomes trust, and how trust becomes defensible value.

Oura’s IPO validates one mature scenario: premium health intelligence supported by recurring revenue.

China tests another: localized integration, regulatory trust, ecosystem behaviour, and lower-friction monetization.

The product may look the same. The commercial logic is not.

This is the lesson for founders and investors far beyond wearables. In the AI era, technology alone does not create defensibility. The moat belongs to those who understand where the market is truly ready to absorb intelligence, pay for it, and build new behaviour around it.

Technology does not scale globally by copying the product. It scales by matching the scenario.

That is Scenario Intelligence.

Are you building at the intersection of hardware, AI, and global markets? Do not wait for a costly market launch to find the fracture in your business model. Reach out to Mans International for a scenario maturity audit of your current product roadmap.