Mans International “Be Your Own Boss” Program is designed to help people from all walks of life around the world who are committed to changing their way of thinking, improving their abilities, and achieving financial freedom and time freedom.

Before You Start

First of all, I’m sorry to tell you that it takes a long time to realize financial freedom and time freedom. If for whatever reason, you have obtained a large amount of wealth, it doesn’t mean that you achieved financial freedom automatically. Because you may not have the ability and psychological capacity to manage large amounts of wealth, the money will be consumed at a rate you can’t imagine.

You might say, can I just ask a financial professional to help me take care of my wealth? The question I asked was do you have the ability to select an outstanding and suitable professional?

If you feel that you ALREADY have independent thinking and various skills, then you do not need to participate in this program! All the best!

Our Values

If you DON’T agree with our values, please do not disturb!

Check Mans International “Be Your Own Boss” program values:

You can either send an email to info@mansinternational.com and we will send you the latest content regularly.

Before You Go

Every year we make plans. Every day we receive tons of information and learn a lot of knowledge, but why most people still can’t make choices that are beneficial to themselves in the long run, achieve their goals, and become a better version of themselves?

本届 WAIC 最让人惊喜的创业故事,不是大厂的重磅发布,也不是实验室的技术突破,而是一个一人公司(OPC)跑出的项目 ——TideFlow AI 个性化睡眠决策系统。

创始人吴松芸没有医学背景,创业的起点只是自己长期受失眠困扰的真实体验。 她的核心洞察很精准:很多人失眠不是环境不好,而是大脑长期处于高唤醒状态,没法自然从清醒过渡到睡眠。TideFlow 用 AI 实时感知用户状态,动态匹配放松音频、呼吸引导等干预方案,帮大脑自然入睡,区别于市面上千篇一律的白噪音、冥想产品。

Your tokens are cheap. Your model is open-source. So what do you actually own?

That question shaped my review of WAIC 2026, held in Shanghai.

More than 1,100 companies presented over 3,000 exhibits. But the real divide was not between larger and smaller models. It was between technologies that attract attention and those approaching defensible, revenue-generating deployment.

WAIC 2026 Shanghai

Over three days, I examined the most relevant medical AI cases through the Mans International SMAF lens: the Scenario Maturity Assessment Framework, which looks beyond model parameters to assess proprietary data, workflow integration, buyer readiness, trust and commercial scalability.

Three trends stood out and they were not equally mature.

Trend 1: The moat moved from the model to the data

Leading companies are no longer applying general models directly to medical questions; they are building “medically enhanced large models” grounded in exclusive data.

A prime example is Baichuan Intelligence’s “Futang·Baichuan’s pediatric model. It was developed with Beijing Children’s Hospital using the clinical expertise of more than 300 paediatric specialists and decades of high-quality, de-identified medical records.

The results are striking: in a head-to-head against 12 attending and resident physicians on 60 real outpatient cases, it hit 91.7% diagnostic accuracy, nearly 15 points above the human average, with 92% medication-safety compliance. It now lives in daily multidisciplinary clinics and is rolled out to 150+ county hospitals in Hebei.

Trend 1: The moat moved from the model to the data

China also presents a compelling initial scenario. Leading paediatric expertise is concentrated in major hospitals, while primary-care and county-level institutions often lack experienced specialists. AI could help distribute medical expertise more widely, not by replacing doctors, but by allowing expert knowledge to travel across institutions and regions.

SMAF read: A static dataset can eventually be copied. A clinical system that improves through validated feedback from each deployment becomes increasingly trusted and harder to replace.

Trend 2: Embodied AI is dazzling — and still maturity-gated

United Imaging Intelligence’s equipment-data-algorithm stack is a real hardware moat that pure software players can’t easily copy. And the humanoid demos were the crowd favorite: Galaxy General’s “AstraBrain” architecture driving a robot through folding laundry and making breakfast; Fourier Intelligence’s GR-3 Care-bot executing a full intent-to-action loop from a spoken “I’m thirsty”; Optics Valley Dongzhi’s “Photon” robots handling patrol, companionship, and health monitoring in elder-care settings.

Trend 2: Embodied AI is dazzling — and still maturity-gated

Impressive. Not yet mature. Getting a robot from a booth into a home or hospital means clearing three hurdles that don’t show up in a product demo:

Safety — the care recipients are disabled or elderly; failure tolerance is close to zero.

Privacy — continuous in-home data collection needs real consent architecture, not a terms-of-service checkbox.

Humanity — the job is care, not just task completion. A robot that folds shirts perfectly but feels clinical hasn’t solved the actual problem.

SMAF read: high potential, low current maturity. This is the category where the technology outpaces the scenario — worth watching, not yet worth pricing as though it’s solved.

Trend 3: Narrow problem, Real payers — OPC models are proving maturity can be earned fast

The most interesting founder story at WAIC wasn’t a lab spinout. TideFlow AI, an “AI personalized sleep decision system” was built solo by Wu Songyun, no medical background, just her own struggle with insomnia.

Trend 3: Narrow problem, Real payers — OPC models are proving maturity can be earned fast

TideFlow’s core insight is that insomnia often stems not from a poor environment, but from a hyperaroused brain. The system uses AI to perceive the user’s state in real-time, dynamically matching intervention plans to help the brain naturally transition into sleep. After 12 iterations, this highly personalized, lightweight business architecture stepped onto the global stage, acquiring real paying users overseas.

SMAF read: this is what fast-tracked maturity looks like — a narrow, well-defined pain point, a founder close enough to it to iterate quickly, and payers who validate the solution before the funding round does.

The Mans International Takeaway

In this profound transformation, the core of industry competition is undergoing a structural reshaping from “Model IQ” to “Scenario EQ.” This is not short-term technological hype; it is a fundamental shift in the logic of value creation, capture, and defense.

Navigating this structural change requires far more than financial reports and model parameters. It demands a precise grasp of regulatory boundaries and a professional analytical framework capable of systematically assessing scenario maturity and identifying strategic gaps. This is precisely the design intent behind the Mans International SMAF.

Ultimately, every medical AI participant must confront a fundamental question: Is your AI strategy designed to win brief applause at the exhibition booth, or to truly crack the real industry dilemma of waiting three hours to see a doctor for five minutes?

If you’re trying to figure out where a specific medical AI bet actually sits on that maturity curve — or how to position a product for international scaling — that’s the exact gap SMAF was built to close. Happy to compare notes.

Mans International applies the Scenario Maturity Assessment Framework to help technology founders and investors distinguish technical readiness from commercial, workflow and ecosystem readiness—particularly across China and international markets.

AI’s Next 99.5% Opportunity: Why the Winners Will Be Built Beyond SaaS

The 0.5% SaaS Trap: AI’s “Pixar Moment”

In the early 1980s, Pixar wasn’t a film studio. It was a struggling hardware company born inside Lucasfilm and backed by Steve Jobs. They built the Pixar Image Computer — a sleek, powerful machine designed for medical imaging and scientific visualization.

Nobody wanted it. No hospitals, no research labs, not even George Lucas. As Pixar bled cash, they had one odd advantage: a tiny in-house team making short animated clips just to demonstrate what the hardware could do. The hardware flopped, but the clips blew people’s minds.

So, Pixar made a radical creative leap: they stopped selling the silicon and started selling the story. They stopped optimizing a tool and reimagined its ultimate purpose. The result was Toy Story, and it rewrote the economics of Hollywood.

The 0.5% SaaS Trap: AI’s “Pixar Moment”

Today, AI founders are facing their own “Pixar moment.” Too many are obsessing over the underlying technology, the tool itself, while missing the grander narrative of the market: delivering undeniable, real-world outcomes.

This fixation has led to what can be called the 0.5% SaaS trap: founders are optimizing for the easiest layer of AI adoption while completely missing the massive 99.5% opportunity waiting in the real economy.

The Canary in the SaaS Coal Mine

Goldman Sachs recently published a sobering metric for the tech ecosystem: software services (SaaS) represent less than 0.5% of global GDP. The remaining 99.5% belongs to the physical world — manufacturing, energy, logistics, healthcare, construction, and robotics.

For the past year, we’ve watched software companies face a massive reality check. The ten largest holdings in a major software ETF collectively shed nearly $800 billion in market cap. This isn’t because software is dying; it’s because AI is breaking the traditional SaaS business model.

The old assumptions — that pricing should be based on user seats, that more users equal more value, or that adding a basic wrapper creates a defensive moat — are collapsing. As autonomous AI agents begin to do the actual work, value is shifting away from software access and moving directly toward trusted, physical outcomes.

The Canary in the SaaS Coal Mine

The capital is already moving. Look at Prometheus, the AI engineering startup backed by Jeff Bezos that recently raised $12 billion at a $41 billion valuation. They aren’t building a better chatbot to write marketing emails; they are building an AI engineer to design physical jet engines and complex industrial systems.

The real battleground is the remaining 99.5% of the economy. But conquering it requires playing by an entirely different set of rules.

The 5 Laws of Industrial AI

In software, an AI hallucination wastes tokens. A confident but wrong AI answer isn’t just a product bug. In industrial settings, it can quickly turn into a trust and liability problem. Goldman Sachs highlights five capabilities that may separate industrial-AI leaders from commoditized competitors:

Physics-Based Architecture: AI must understand materials, motion, temperature and mechanical constraints — not just language.

Proprietary Operational Data: The strongest moats will come from private deployment data, including failures, edge cases and real-world operating patterns.

Edge Deployment: Critical systems cannot depend entirely on cloud connectivity. Intelligence must often run locally for speed, reliability and safety.

Certifiability: In regulated environments, technical performance is insufficient. The system must be demonstrably predictable, controllable and safe.

Workflow Integration: Customers will not rebuild their operations around a new tool. The highest-value AI becomes a seamless capability layer inside existing workflows.

The Hidden Risk: Is Your Scenario Mature?

Goldman Sachs maps the technical requirements for the real economy. But for founders and investors, technical readiness is only half the battle. The greater risk is commercial readiness.

This is where the Scenario Maturity Assessment Framework (SMAF) becomes essential.

A technology can perform brilliantly and still fail to scale because the commercial environment around it is not ready. When industrial AI stalls, the problem is often not the product itself, but the scenario in which it is being applied. Three questions expose the gap:

The Buyer & Budget: Are you selling to a specific operational buyer with a P&L, or pitching “abstract efficiency” that no single department actually owns?

The Integration Friction: Can the product fit into existing operations, or must the customer redesign its workflow before receiving value?

The Value Capture: Are you selling software access to an industrial buyer who only cares about measurable operational and financial outcomes?

Remember Pixar? Their Image Computer was technically brilliant. But the scenario was immature. They were applying a world-class capability to the struggling hardware scenario — until they pivoted to a more valuable outcome: computer-generated storytelling.

The next generation of AI winners will not necessarily have the most sophisticated models. They will be the companies that translate AI into outcomes that are trusted, workflow-integrated and commercially measurable.

When the technology works but adoption and revenue stall, do not immediately assume the product has failed. Audit the scenario.

At Mans International, we help deep-tech founders and investors identify where commercialization is breaking down—whether the answer is stronger workflow integration, a better value-capture model or a more mature market application.

Here is the signal most founders and investors missed:

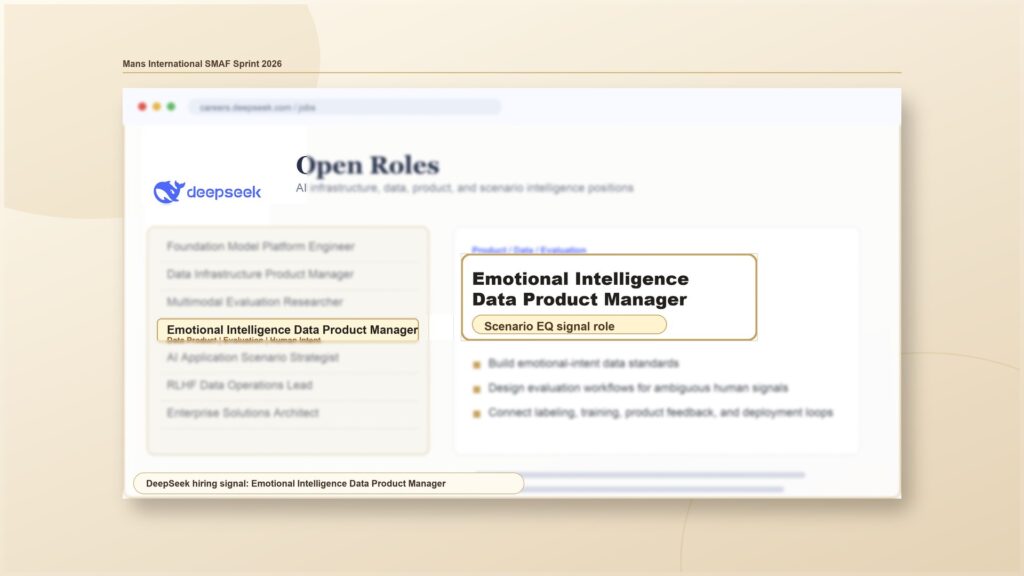

A Chinese AI company reportedly raised US$7.4 billion at around a US$50 billion valuation, cracking the global top 15 unicorns.

That company is DeepSeek — one of China’s most watched AI labs, known for challenging the global AI race with high-performing, cost-efficient large language models.

Yet after reportedly closing a massive funding round of over US$7.4 billion, or 50 billion RMB, its immediate next move was not simply a public computing-power expansion or another race to cut parameter costs. Instead, it launched a comprehensive hiring wave across 7 categories and 33 roles.

Among them, one role deserves particular attention from founders and investors: Emotional Intelligence Data Product Manager.

The core responsibility of this role is about turning complex, ambiguous human emotions and intentions into evaluation systems, training workflows, and product feedback loops.

The Next AI Battle Is Not Only Model IQ. It Is Scenario EQ.

Through the lens of SMAF — Scenario Maturity Assessment Framework, our active framework to stress-test an AI company’s commercial ecosystem and value-capture architecture, DeepSeek’s hiring signal points to a deeper shift:

The next phase of AI commercialization will not be won only by higher model IQ. It will be won by stronger scenario EQ.

Can the AI detect when a customer is truly angry? Can it understand when a patient says “I’m fine,” but is actually anxious, confused, or losing trust? Can it recognize when a buyer says “let us think about it,” but the real blocker is budget, internal politics, risk perception, or cultural mismatch?

These are not simple sentiment-analysis problems. They are scenario-maturity problems.

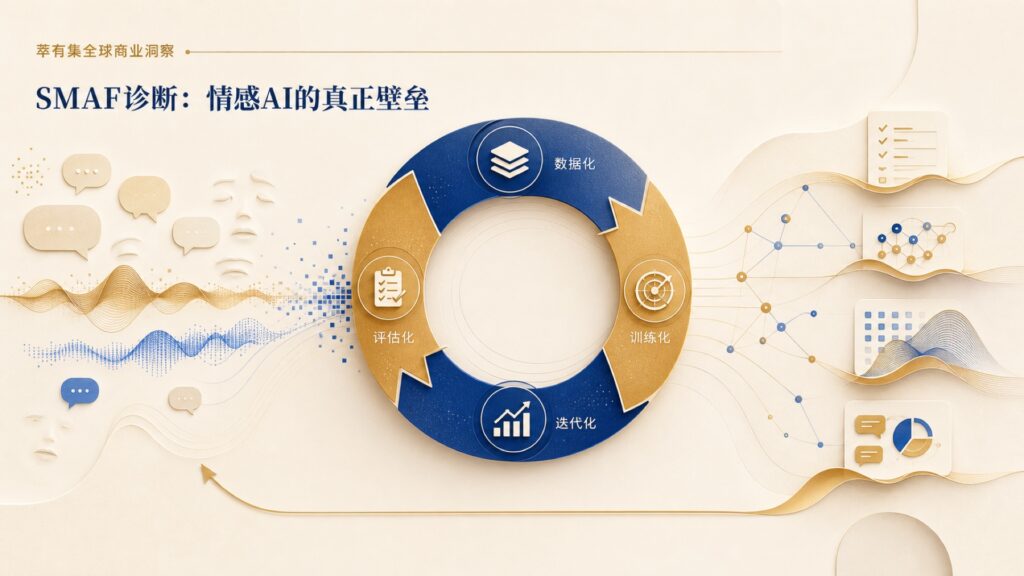

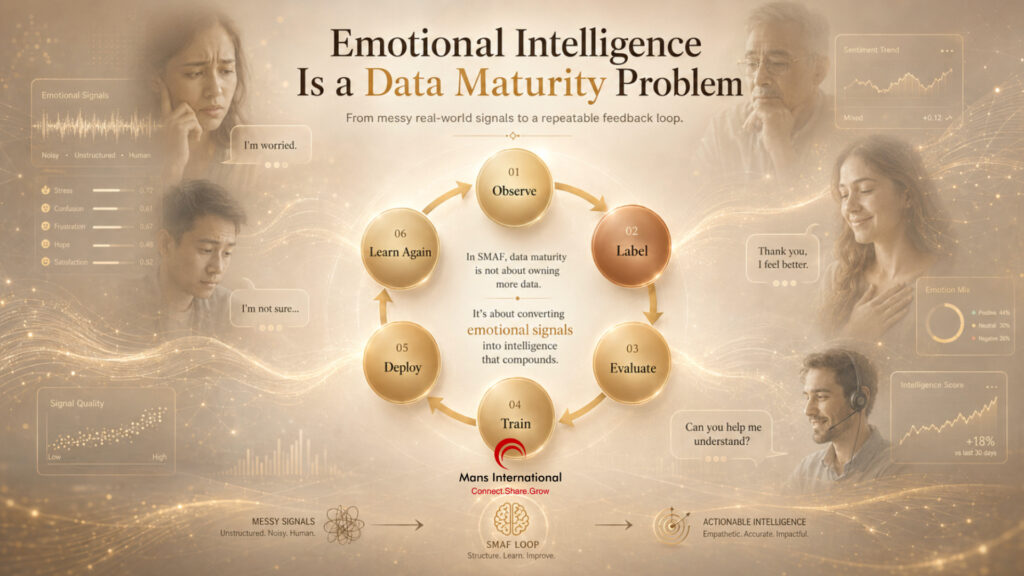

Emotional Intelligence Is a Data Maturity Problem

In SMAF, data maturity does not mean owning more data. It means the ability to convert messy, fragmented, non-standard signals from real use cases into a repeatable loop:

This is precisely why the “Emotional Intelligence Data Product Manager” is an essential marker for founders and institutional investors. This is not an abstract, soft-skill humanities role; it is a hard commercial signal. AI is graduating from the basic tool phase of answering questions to the complex scenario phase of decoding human intent.

Furthermore, as AI leaders shift from model-centric competition to usage-efficiency and token-economics discipline, scenario accuracy becomes a direct P&L issue. High Scenario EQ means fewer wasted interactions, fewer misinterpreted prompts, fewer repeated explanations, and fewer costly friction loops.

In enterprise AI, understanding the scenario correctly is not merely a product advantage but a path to more sustainable profitability.

The Mans International View: East–West Scenario Splintering

Technology may travel globally, but emotional intelligence does not move across markets in a straight line.

The same underlying model capability can face completely different maturity paths in North America, China, and other markets. I call this Scenario Splintering: when one technology enters different cultural, regulatory, workflow, and business environments — and each environment demands a different product logic.

The US Paradigm (Persona & Deep Alignment): Pioneers like Character.ai and Replika established an early blueprint for highly individualized relationship building, utilizing Conversation Designers, Psychology Researchers, and Dialogue Data Experts to curate explicit “personas” and empathetic baselines.

The China Paradigm (Rapid Vertical Embedding): Domestic players like Emoha (聆心智能) trained models directly on clinical counseling data to deploy its series across over 600 specific mental health, university, and enterprise scenarios. Following its integration with Zhipu to power CharacterGLM, the priority shifted to cross-ecosystem scale — immediately embedding empathetic capabilities into gaming NPCs, virtual companions, and digital human assets to maximize immediate commercial velocity.

The Strategic Trap: Copy-pasting Western “clinical AI” to the East usually dies because users won’t pay for a “diagnostic” experience. Pushing Eastern “heavy-companion AI” to the West usually dies under privacy scrutiny. Cross-border Emotional AI requires Scenario Reconstruction (Cultural Translation), not just code translation.

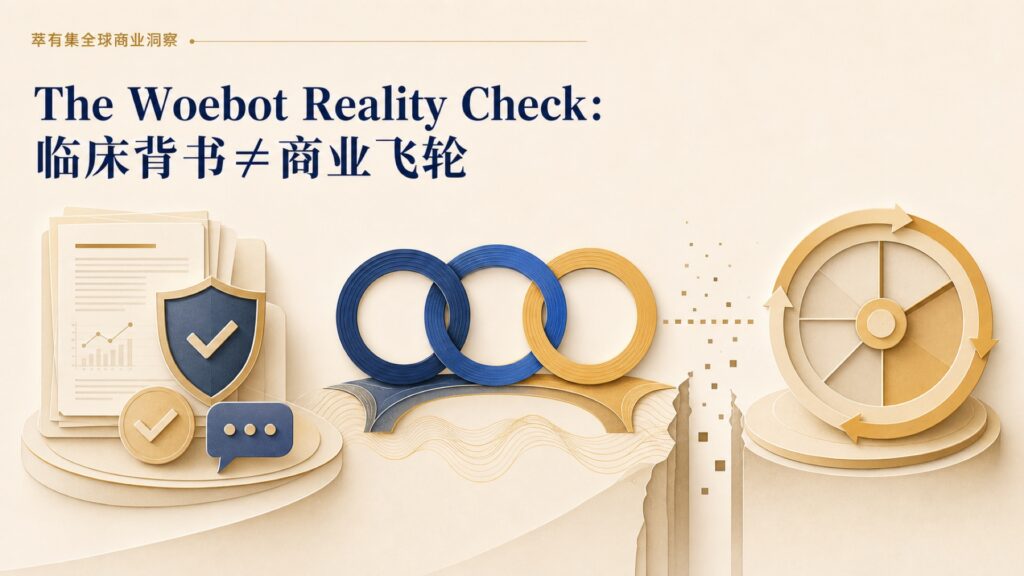

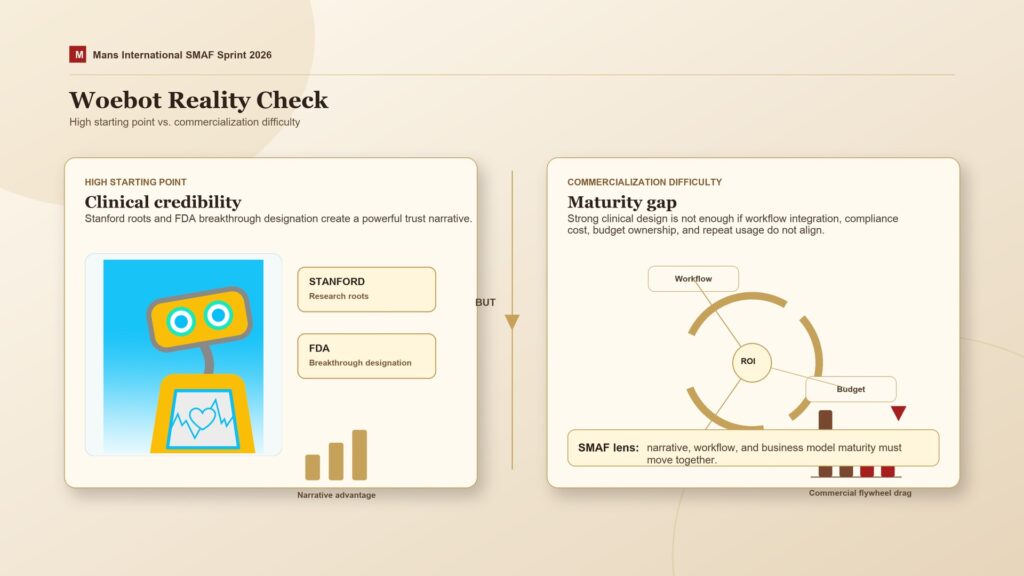

The Woebot Reality Check

Look at Woebot Health. Despite its Stanford roots and FDA breakthrough designation, it has struggled to build a sustainable commercial flywheel.

Under the SMAF lens, this is a classic case of misalignment in narrative, workflow, and business model maturity. While their clinical narrative was strong, their workflow maturity struggled to seamlessly integrate into existing fragmented healthcare systems, and their business model faced friction reconciling the high costs of medical compliance with shifting B2B enterprise budgets. Having the best clinical design doesn’t matter if the commercial scenario isn’t mature enough to sustain the business.

Execution is becoming easier. Scenario Intelligence is becoming more valuable.

At Mans International, this is the core of our SMAF work: helping founders, investors, and cross-border technology teams evaluate whether a promising AI product has matured enough to become a real commercial system.

If you are currently building the next generation of affective interfaces, or orchestrating a cross-border tech launch between Western innovation and Eastern scale, look beyond the leaderboard benchmarks.

Contact Mans International to schedule a private, selective Scenario Maturity Audit. Let’s assess your structural gaps and secure your commercial roadmap before your next major deployment.

The I Ching (Book of Changes) states: “Heaven’s movement is ever vigorous; thus, the noble person constantly strives for self-improvement.” This underlying force of relentless self-renewal, regardless of the circumstances, has found its most extreme validation in the practice of Mr. Cai Lei.

An ALS breakthrough: A master class in Deep-Tech Ecosystem Building, Founder Resilience, and SMAF

In 2019, Mr. Cai Lei, a former vice president of JD.com and one of the pioneers behind China’s electronic invoice system, was diagnosed with amyotrophic lateral sclerosis, or ALS. He was 41. He had just welcomed a new child. His career, family, and life were all at a peak moment.

Then came the diagnosis. ALS is often described as one of the most devastating neurodegenerative diseases. The average survival window after diagnosis is often only a few years.

Seven years later, in 2026, his body function score plummeted from 48 to 4. He is completely paralyzed from the neck down, his vocal cords have severely atrophied, and he relies on a liquid diet and a 24-hour ventilator to survive. Across his entire body, only his eyes remain under his autonomous control.

Cai Lei before and after ALS

Yet, Cai Lei’s story is far more than an inspiring narrative of resilience and empathy. Analyzed through the Scenario Maturity Assessment Framework (SMAF), it stands as a textbook masterclass in deep-tech scenario breakthroughs. It is a blueprint of how to take a globally recognized “unsolvable dead end” and reconstruct it into a high-maturity, self-sustaining ecosystem of research collaboration and commercial translation.

I. Deconstructing the Breakthrough via SMAF: A High-Maturity Super Ecosystem

At Mans International, we utilize the SMAF (Scenario Maturity Assessment Framework) to evaluate the commercial viability and translation potential of deep tech ventures. We have seen too many projects perish in the “slide deck” phase or or “lab-only self-indulgences.”

From a scenario maturity perspective, the true brilliance of Cai Lei’s “ice-breaking” initiative is not simply his unwavering belief, but his methodical execution. He took a highly fragmented, chronically inefficient rare-disease scenario — one lacking adequate resource attention — and orchestrated it into a synchronized system uniting patients, data, research, clinical trials, capital, AI, and public trust.

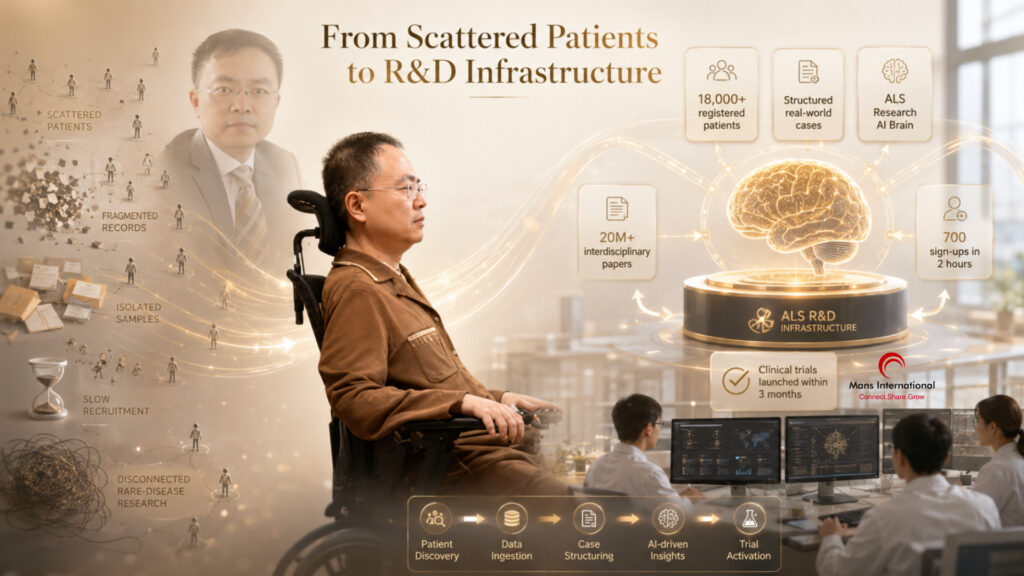

1. Data and Workflows: From Scattered Patients to R&D Infrastructure

One of the greatest bottlenecks in rare disease R&D is scattered patient populations, scarce biological samples, and a lack of real-world data. Often, research does not lack direction; it lacks a stable, continuous, and actionable data foundation.

The Data Engine: Cai Lei built the “Jianyu Mutual Aid Home,” the world’s largest civilian ALS research database (over 18,000 registered users), housing tens of thousands of structured real-world cases. He also launched an “ALS Research AI Brain,” training 24/7 on over 20 million interdisciplinary papers to automatically filter and evolve targets without burdening researchers.

The Workflow: This 360-degree dynamic vital-sign tracking system compresses notoriously slow clinical recruitment to astonishing speeds — achieving “hour-level” responsiveness (i.e. 700 sign-ups in 2 hours; launching clinical trials within 3 months).

Data and Workflows: From Scattered Patients to R&D Infrastructure

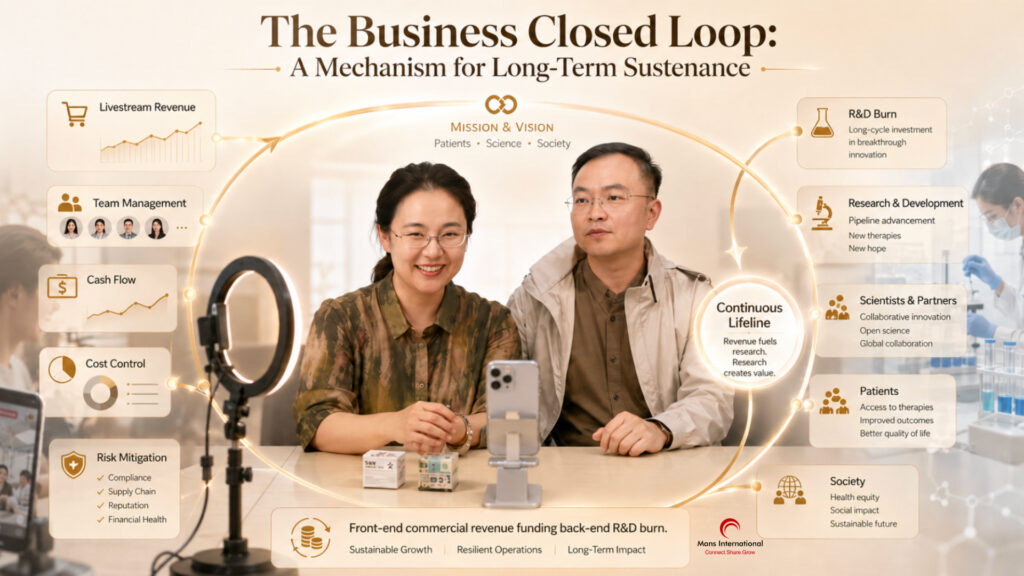

2. The Business Closed Loop: A Mechanism for Long-Term Sustenance

Rare disease research cannot survive solely on short-term donations or one-off grants. Drug discovery features long cycles, high failure rates, and relentless capital demands, while external funding environments and public attention fluctuate. Without a stable financial engine, even the grandest mission will bleed out mid-way.

The partnership forged between Cai Lei and his wife, Duan Rui, perfectly demonstrates the synergy of vision and operations. Many view Duan Rui’s live-streaming efforts purely as a “wife’s sacrifice.” While deeply moving and true, from a strategic perspective, it is a brilliantly designed commercial closed loop.

Cai Lei continually raises the ceiling of their mission — connecting patients, scientists, pharma, and society. Meanwhile, Duan Rui absorbs the immense operational realities: live-streaming revenue, team management, cash flow, cost control, and risk mitigation. This closed-loop of “front-end commercial revenue funding back-end R&D burn” provides a continuous lifeline for a highly uncertain, long-cycle scientific endeavour.

The Business Closed Loop: A Mechanism for Long-Term Sustenance

3. Narrative & Ecosystem: Evolving from Empathy to Industry Consensus

Before Cai Lei, ALS was trapped in a weak narrative within public and industry discourse — viewed merely as an “incurable and unprofitable” tragedy. It garnered generalized sympathy but lacked actionable pathways.

Cai Lei elevated this narrative fundamentally. He did not stop at emotional appeals for awareness; he broke down rare-disease R&D into actionable industry propositions. He allowed the scientific community, the biotech industry, and the public to clearly see their specific roles and value.

This mature narrative has penetrated industry silos, uniting over 60 global research teams and 50+ biotech companies, transforming an untouched “cold sector” into a highly coordinated battlefield with shared consensus, pooled resources, and a synchronized tempo.

Narrative & Ecosystem: Evolving from Empathy to Industry Consensus

II. The Founder’s Mirror: Resilience for Global Founders

In his recent “Countdown” speech on Global ALS Day, June 21, 2026, Cai Lei said he had already defeated an enemy more terrifying than ALS: despair.

For founders today — navigating agonizing market cycles and high-stakes survival tests — Cai Lei’s mental fortitude serves as a profound mirror:

Reject the Victim Mentality. Complaining about the macro environment or the “capital winter” yields zero value. Completely paralyzed and unable to speak, Cai Lei never wallowed in the unfairness of fate. He immediately pivoted his strategy, utilizing an eye-tracking device to launch a race against time. Radical acceptance and execution to the absolute limit are the foundational ethics of a founder.

Pry Open Incremental Gaps in Dead Ends. Cai Lei noted: “You might think there is only a solid wall in front of you. But look down, there might be a path; turn sideways, there is a gap. You can even choose to climb over or dig through.” When traditional funding tightens and cross-border barriers rise, a founder’s core competency is leveraging tools — like AI and cross-disciplinary ecosystems — to pry open growth spaces ignored by the mainstream.

Anchor Your Venture in a Grand Proposition.“The best way to overcome fear is to place yourself within a much greater cause.” When your corporate vision is tied to core societal challenges — hard tech breakthroughs, life sciences, energy transitions — the resilience you unlock will far surpass what secular fame or profit can sustain.

Pry Open Incremental Gaps in Dead Ends

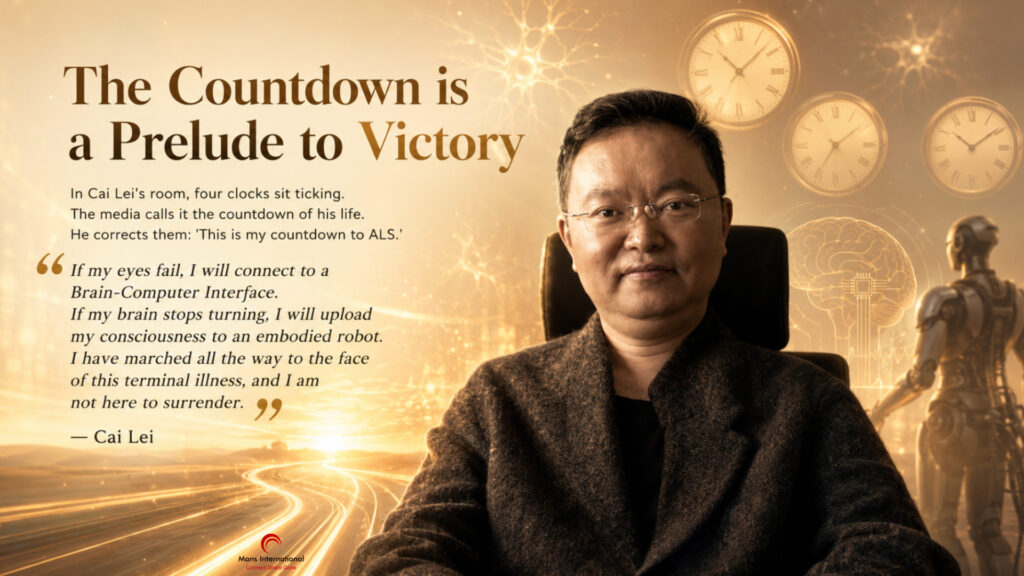

III. Conclusion: The Countdown is a Prelude to Victory

In Cai Lei’s room, four clocks sit ticking. The media calls it the countdown of his life. He corrects them: “This is my countdown to ALS.”

“If my eyes fail, I will connect to a Brain-Computer Interface. If my brain stops turning, I will upload my consciousness to an embodied robot. I have marched all the way to the face of this terminal illness, and I am not here to surrender.”

As heaven’s movement is ever vigorous, so must a leader ceaselessly strive along.

The Countdown is a Prelude to Victory

Here is to all the founders who keep walking through the valleys of economic cycles. Here is to the researchers grinding relentlessly in their labs. Here is to all those who refuse to bow to fate.

Do not ask where the hope lies. Keep moving forward, and hope will reveal itself. As long as you do not retreat, every direction is the way forward.

Global Strategic Partnership

Leading global research institutions, multinational pharmaceutical companies, biotech innovators, and international funds are invited to partner with Mans International to access and navigate high-maturity life science and deep-tech ecosystems.

Through our SMAF — Scenario Maturity Assessment Framework — we help identify where technology, capital, clinical resources, market readiness, and ecosystem trust can be precisely aligned.

Our goal is to reduce cross-border and cross-sector friction, accelerate clinical and commercial translation, and support breakthrough technologies and strategic capital in moving from promise to real-world impact.

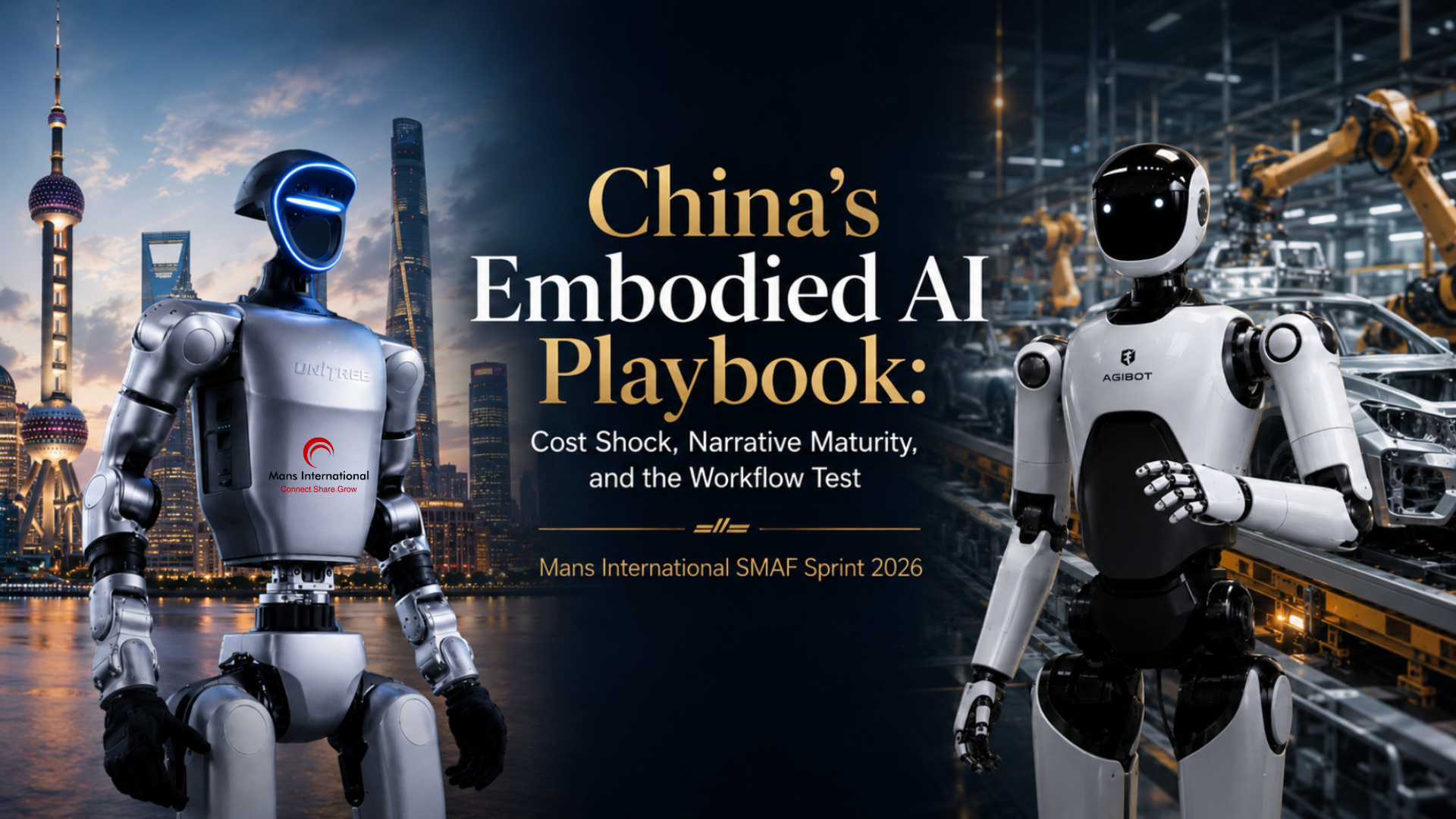

While Elon Musk packages “infrastructure + AI” into a grand capital narrative, China’s humanoid robotics sector is executing a dual-track playbook.

Unitree drives the market through cost disruption. Agibot drives it through strategic narrative and embodied intelligence.

Through the Scenario Maturity Assessment Framework, or SMAF, these two companies are not just robotics competitors. They represent two different answers to the same strategic question: How does a humanoid robot move from technical spectacle to commercial readiness?

Playbook A: Unitree’s “Cost Shock”

Unitree’s breakthrough is industrial, not just technical.

Leveraging China’s mature electric vehicle (EV) supply chain, they’ve driven humanoid pricing below $20,000 — shifting the market psychology from “futuristic tech demo” to “purchasable hardware.”.

In SMAF terms, this reflects world-class execution in Supply Chain Maturity and Commercial Disruption Potential. It lowers the barrier for widespread developer experimentation while forcing high-cost global competitors onto the defensive.

Unitree’s “Cost Shock”

However, cheap hardware does not guarantee a valuation premium. For enterprise buyers, the real question is:

Can it work reliably inside my operation, reduce labor burden, avoid safety issues, integrate with existing systems, and produce measurable ROI?

If a robot requires a human “babysitter” to constantly reset, maintain, or supervise it, the ROI evaporates.

The real cost isn’t the hardware. It’s the operational burden.

Unitree’s next survival test: Can we make it reliable enough that customers never regret deploying it?

Playbook B: Agibot’s Narrative-Maturity Bet

Rather than competing purely on cost, Agibot is leading with an embodied AI vision: robots that learn, adapt, and improve through real-world deployment.

In SMAF terms, Agibot exhibits strong Narrative Maturity — the ability to translate complex technology into a credible, investable story about AI entering the physical world.

Agibot’s Narrative-Maturity Bet

Its maturity profile looks very different from Unitree’s:

Narrative Maturity: Strong. Positioning embodied AI as a new intelligence layer for physical work is easy for investors to grasp, granting Agibot a higher valuation ceiling.

Workflow Maturity: Testing. Agibot is moving from demos to real industrial environments to expose hidden frictions. However, field training is not scenario maturity. Performing a single task creates excitement; becoming a reliable, low-friction production tool creates purchasing confidence.

Business Maturity: Expectation-Driven. Agibot’s commercial viability hinges on a Starlink-style data flywheel: deployment → task data → better intelligence → broader deployment. If successful, they are not just selling hardware — they are building a compounding intelligence system.

The SMAF Strategic Warning: The higher the narrative maturity, the greater the pressure for scenario validation. A compelling story secures capital, but it cannot permanently replace workflow proof.

The Cultural Bridge: Why These Two Paths?

These playbooks reflect two deeper instincts within China’s technology ecosystem:

Unitree represents supply-chain alchemy. Forged in China’s brutal EV price wars, Forged in the brutal NEV price wars, it turns mature industrial capacity into a global price shock. Unitree is trying to win by industrializing the body.

Agibot represents leapfrog ambition. Aligned with national priorities for AI-driven industrial upgrades, Agibot bets that software and data can compress years of mechanical refinement. They are attempting to win by accelerating the brain.

While one path begins with manufacturing maturity and the other with intelligence ambition, both eventually face the same question: Can the robot become useful inside real workflows?

The Imperative for Founders and Investors

Cost shocks open markets. Narrative maturity lifts valuation ceilings. Data loops create compounding power. But both companies must ultimately achieve Workflow Maturity — the threshold where demos become adoption, deployment earns trust, and technology justifies a valuation premium.

The Imperative for Founders and Investors

The Lesson for Founders:

Do not confuse technical capability with commercial readiness.

Do not confuse low cost with customer value.

Do not confuse a strong narrative with scenario maturity.

Do not confuse deployment with true adoption.

The Diligence Test for Investors:

Which company is not just building a better machine, but entering the more mature scenario?

Valuation power won’t belong to the cheapest robot or the most ambitious story. It will belong to the company that proves its robot reduces friction and generates measurable ROI.

That is the core lesson of China’s dual-track embodied AI playbook.

And it is exactly why I built the Scenario Maturity Assessment Framework (SMAF): to help founders and investors identify the gap between technical ambition and scenario maturity before the market does.