Mans International SMAF Sprint 2026

The I Ching (Book of Changes) states: “Heaven’s movement is ever vigorous; thus, the noble person constantly strives for self-improvement.” This underlying force of relentless self-renewal, regardless of the circumstances, has found its most extreme validation in the practice of Mr. Cai Lei.

In 2019, Mr. Cai Lei, a former vice president of JD.com and one of the pioneers behind China’s electronic invoice system, was diagnosed with amyotrophic lateral sclerosis, or ALS. He was 41. He had just welcomed a new child. His career, family, and life were all at a peak moment.

Then came the diagnosis. ALS is often described as one of the most devastating neurodegenerative diseases. The average survival window after diagnosis is often only a few years.

Seven years later, in 2026, his body function score plummeted from 48 to 4. He is completely paralyzed from the neck down, his vocal cords have severely atrophied, and he relies on a liquid diet and a 24-hour ventilator to survive. Across his entire body, only his eyes remain under his autonomous control.

Yet, Cai Lei’s story is far more than an inspiring narrative of resilience and empathy. Analyzed through the Scenario Maturity Assessment Framework (SMAF), it stands as a textbook masterclass in deep-tech scenario breakthroughs. It is a blueprint of how to take a globally recognized “unsolvable dead end” and reconstruct it into a high-maturity, self-sustaining ecosystem of research collaboration and commercial translation.

I. Deconstructing the Breakthrough via SMAF: A High-Maturity Super Ecosystem

At Mans International, we utilize the SMAF (Scenario Maturity Assessment Framework) to evaluate the commercial viability and translation potential of deep tech ventures. We have seen too many projects perish in the “slide deck” phase or or “lab-only self-indulgences.”

From a scenario maturity perspective, the true brilliance of Cai Lei’s “ice-breaking” initiative is not simply his unwavering belief, but his methodical execution. He took a highly fragmented, chronically inefficient rare-disease scenario — one lacking adequate resource attention — and orchestrated it into a synchronized system uniting patients, data, research, clinical trials, capital, AI, and public trust.

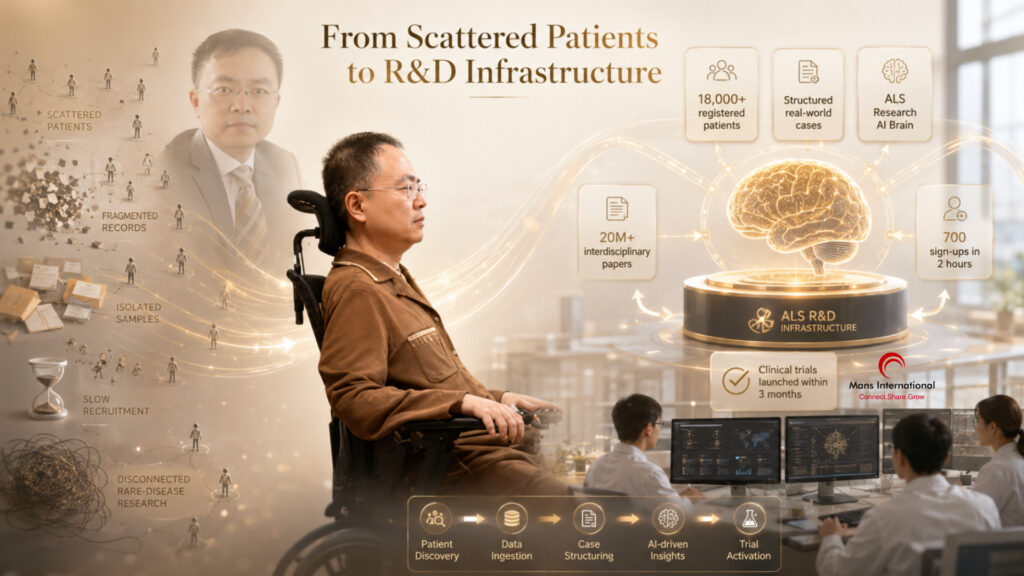

1. Data and Workflows: From Scattered Patients to R&D Infrastructure

One of the greatest bottlenecks in rare disease R&D is scattered patient populations, scarce biological samples, and a lack of real-world data. Often, research does not lack direction; it lacks a stable, continuous, and actionable data foundation.

- The Data Engine: Cai Lei built the “Jianyu Mutual Aid Home,” the world’s largest civilian ALS research database (over 18,000 registered users), housing tens of thousands of structured real-world cases. He also launched an “ALS Research AI Brain,” training 24/7 on over 20 million interdisciplinary papers to automatically filter and evolve targets without burdening researchers.

- The Workflow: This 360-degree dynamic vital-sign tracking system compresses notoriously slow clinical recruitment to astonishing speeds — achieving “hour-level” responsiveness (i.e. 700 sign-ups in 2 hours; launching clinical trials within 3 months).

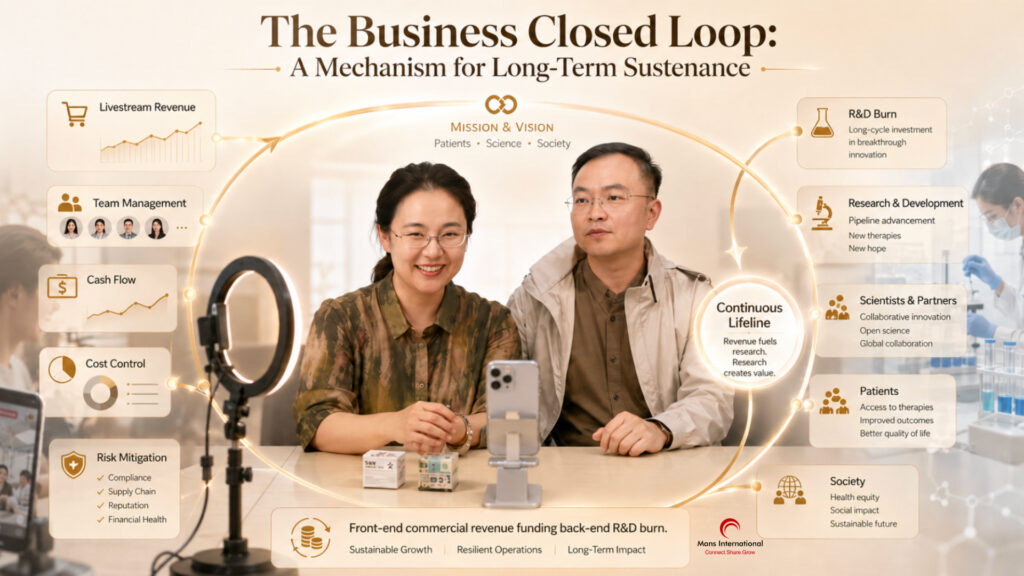

2. The Business Closed Loop: A Mechanism for Long-Term Sustenance

Rare disease research cannot survive solely on short-term donations or one-off grants. Drug discovery features long cycles, high failure rates, and relentless capital demands, while external funding environments and public attention fluctuate. Without a stable financial engine, even the grandest mission will bleed out mid-way.

The partnership forged between Cai Lei and his wife, Duan Rui, perfectly demonstrates the synergy of vision and operations. Many view Duan Rui’s live-streaming efforts purely as a “wife’s sacrifice.” While deeply moving and true, from a strategic perspective, it is a brilliantly designed commercial closed loop.

Cai Lei continually raises the ceiling of their mission — connecting patients, scientists, pharma, and society. Meanwhile, Duan Rui absorbs the immense operational realities: live-streaming revenue, team management, cash flow, cost control, and risk mitigation. This closed-loop of “front-end commercial revenue funding back-end R&D burn” provides a continuous lifeline for a highly uncertain, long-cycle scientific endeavour.

3. Narrative & Ecosystem: Evolving from Empathy to Industry Consensus

Before Cai Lei, ALS was trapped in a weak narrative within public and industry discourse — viewed merely as an “incurable and unprofitable” tragedy. It garnered generalized sympathy but lacked actionable pathways.

Cai Lei elevated this narrative fundamentally. He did not stop at emotional appeals for awareness; he broke down rare-disease R&D into actionable industry propositions. He allowed the scientific community, the biotech industry, and the public to clearly see their specific roles and value.

This mature narrative has penetrated industry silos, uniting over 60 global research teams and 50+ biotech companies, transforming an untouched “cold sector” into a highly coordinated battlefield with shared consensus, pooled resources, and a synchronized tempo.

II. The Founder’s Mirror: Resilience for Global Founders

In his recent “Countdown” speech on Global ALS Day, June 21, 2026, Cai Lei said he had already defeated an enemy more terrifying than ALS: despair.

For founders today — navigating agonizing market cycles and high-stakes survival tests — Cai Lei’s mental fortitude serves as a profound mirror:

- Reject the Victim Mentality. Complaining about the macro environment or the “capital winter” yields zero value. Completely paralyzed and unable to speak, Cai Lei never wallowed in the unfairness of fate. He immediately pivoted his strategy, utilizing an eye-tracking device to launch a race against time. Radical acceptance and execution to the absolute limit are the foundational ethics of a founder.

- Pry Open Incremental Gaps in Dead Ends. Cai Lei noted: “You might think there is only a solid wall in front of you. But look down, there might be a path; turn sideways, there is a gap. You can even choose to climb over or dig through.” When traditional funding tightens and cross-border barriers rise, a founder’s core competency is leveraging tools — like AI and cross-disciplinary ecosystems — to pry open growth spaces ignored by the mainstream.

- Anchor Your Venture in a Grand Proposition. “The best way to overcome fear is to place yourself within a much greater cause.” When your corporate vision is tied to core societal challenges — hard tech breakthroughs, life sciences, energy transitions — the resilience you unlock will far surpass what secular fame or profit can sustain.

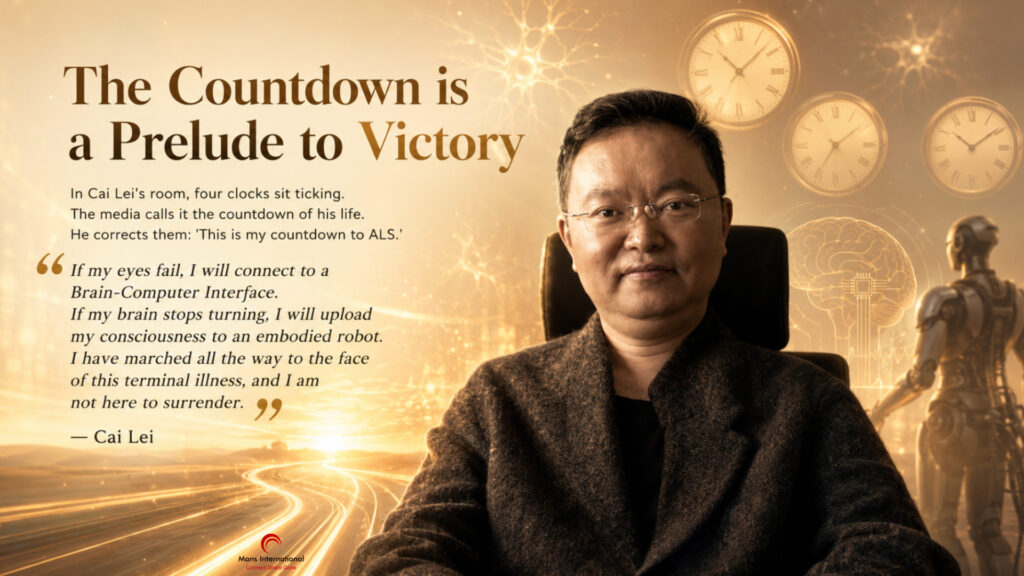

III. Conclusion: The Countdown is a Prelude to Victory

In Cai Lei’s room, four clocks sit ticking. The media calls it the countdown of his life. He corrects them: “This is my countdown to ALS.”

“If my eyes fail, I will connect to a Brain-Computer Interface. If my brain stops turning, I will upload my consciousness to an embodied robot. I have marched all the way to the face of this terminal illness, and I am not here to surrender.”

As heaven’s movement is ever vigorous, so must a leader ceaselessly strive along.

Here is to all the founders who keep walking through the valleys of economic cycles. Here is to the researchers grinding relentlessly in their labs. Here is to all those who refuse to bow to fate.

Do not ask where the hope lies. Keep moving forward, and hope will reveal itself. As long as you do not retreat, every direction is the way forward.

Global Strategic Partnership

Leading global research institutions, multinational pharmaceutical companies, biotech innovators, and international funds are invited to partner with Mans International to access and navigate high-maturity life science and deep-tech ecosystems.

Through our SMAF — Scenario Maturity Assessment Framework — we help identify where technology, capital, clinical resources, market readiness, and ecosystem trust can be precisely aligned.

Our goal is to reduce cross-border and cross-sector friction, accelerate clinical and commercial translation, and support breakthrough technologies and strategic capital in moving from promise to real-world impact.